Gordon Parks, Untitled Fashion Photograph, c. 1960s

DAY 14 Today is Monday, January 16,th and we are studying the twenty-first century phenomenon of art investment funds.

Our particular case study is the Tosca Photography Fund, for which you have the 2010 annual report. But also check out

the chapter from Horowitz on Art Investment Funds (and the accompanying appendix). In your response to the reading,

imagine/design your own art investment fund with sample work (s) and strategies.

Readings

Art of the Deal: Chapter 3

ARTH 4696 FINLEY Art Investment Funds HOROWITZ.pdf

Art of the Deal: Appendix C

ARTH 4696 FINLEY Appendix C Art Investment Fund Universe HOROWITZ.pdf

Tosca Photography Fund Year End Report

Tosca Photography 2011 fund review.pdf

Individual Contributions

The art market is on a very interesting trend. From a relatively esoteric beginning in which transactions were relationship based between few, established buyers and sellers, the globalization of the art world has produced a more structure marketplace with greater transparency, liquidity, and visibility in the eyes of the investing public. Art funds, in theory, are in a unique position to profit from the appreciation of art and the current bull market, as they possess several distinct advantages to dealers: they are capable of lower costs and overhead, as they don't require large exhibition spaces, they can employ a broad selection of expertise (unlike dealers who often specialize), the large capital bases provide unprecedented purchasing power, and longer, buy and hold investment horizons are possibly the ideal way to invest in art. Art is very unique, in that it a superior good (meaning as wealth increases, demand for the product increases) yet it is highly uncorrelated with other popular investment vehicles. The fluctuations of the stock market has little connection wit hthe art market, and demand has often been sustained in times of economic recessions. The primary factor behind this sustained bull market is the prestige element in art investing, in that art carries a significant value in its signaling of wealth and status, factors that don't disappear with the economy. The wealthiest portion of the consumer base will always have a very strong desire to signal their status, and won't be as susceptible to market volatility, creating a very stable and sustained demand base. As a result, many high-profile, high-price transactions have produced widespread public interest in the art market -- while these sales may not be indicative of the larger market, their volatility creates consumer confidence and interest, which is ultimately the largest and most significant driver of value in an industry in which the product -- art -- produces no actual cash flows to its owner. Many of the costs are sunk, and lie in transaction, storage, shipping, and insurance expenses -- these expenses are no doubt inflated, as there are many inefficiencies in the relatively young art investment market, such as conflicts of interests in transactions and large information asymmetries. Moreover, the only real opportunity to realize an investment lies in its resale. While the resale value is a relatively riskless investment, often the investment horizons required to fully ensure this value are much longer than time periods investors are comfortable with, especially as holding art during the time period can be cash flow negative. Prices are opaque, hard to predict and quantify, and subject to buyer's preferences, which further makes resale value difficult to ensure. The combination of these factors represent significant obstacles for an investment fund concentrated on art. One can infer that art, as part of a diversified portfolio of assets, works best when it is used as a hedge against other facets such as debt or equity, due to its low correlation with these investment vehicles and its ability to weather bearish markets. What seems fascinating is that most investment theses concern products that carry inherent monetary value, have easily agreed upon valuations due to concrete monetary cash flows and discounted cash flow analyses, and are traded in a market with sufficient liquidity to ensure resale and consumer confidence. Not only does art fail to satisfy these requirements, but its very value depends in its uniqueness and scarcity. If art funds and investment strategies succeed in becoming mainstream and ubiquitous, the result will be the commercialization of art, the mass increase in its production to meet the rise in demand, and its eventual homogeneity as arbitrage and mass scrutiny eliminate inefficiences and equalize differences in value. This very process of commercialization will ultimately destroy the scarcity and uniqueness of art, and thus its value; as art funds experience success, they will proliferate, and art will become homogeneous, and thus diminish in value as a signal of prestige and an aesthetic decorative piece, and thus the very investment funds which seek to profit off art's value will ultimately destroy it. In short, the process of the commercialization of the art market can ultimately lead to its demise -- art cannot function as a consumer product, as it provides no cash flow and has no truly functional value. For it to continue is success, it must maintain lower levels of supply and scarcity, which will be difficult to ensure as its popularity as an investment grows.

I don't think I would create a purely art-focused investment fund. I think there are inefficiencies to be exploited in art, but the time horizons required to fully maximize returns are prohibitive. Even in the past, when art funds have taken fully advantage of bull markets, their inflation-adjusted annualized returns and IRR's have been marginal, and may not offset opportunity costs. It is difficult to fully gauge market trends, and opportunity-based strategies would be subject to higher volatility. Middlemen such as auction houses take large cuts of returns, and there are many instances of conflicts of interest in the marketplace prohibiting a fully competitive or efficient market. Art in and of itself provides no cash flows to buffer market downturns, and sunk costs are considerable and unavoidable. Some firms have opted to vertically integrate, identifying good artists at young, cheap stages in their careers in the hopes of value appreciation, or investing in one medium in one geographic setting at all stages of production, but even this strategy poses fundamental problems, as art ultimately acquires value through its increase in public perception, eye-catching sales prices, and inclusion in art magazines and critical analyses -- a buy and hold strategy effectively takes art off the market, and thus prohibits it from acquiring reputation and marketing capital through public acknowledgement. Furthermore, any success is likely to produce many copycat funds and entrants to the market, which will further reduce returns. If I had to include art as an investment -- I do think it is valuable, as there are inefficiencies to exploit, strong recent upward market trends, and negative correlations leading to high hedge value in portfolios -- it will be as a part of the diversification process in a larger fund that includes equity, fixed-income investments, and other investment vehicles.

Throughout history, there have been numerous attempts by the financial sector to make money from the successful appreciation of art investments. However, as the readings seem to indicate, this is a very risky business which has not seen much success. Despite this, art investment funds have recently seen a revival of sorts in the 21st century. The art market is turning towards commodification as it never has before, and many investors see this as an opportunity to get in early and earn high levels of profit by strategic buying and selling plans. Unfortunately, this practice has really not become much less risky as one can see in the large number of abandoned funds in the early 2000s. The problem with the market's stability is partially due to the inefficiencies of the market and also the distinctly different way that art is valued as compared to many other categories of assets. Art can be tricky to value because it is worth what someone is willing to pay for it at the time. Its price is also not an island unto itself. The price of an art work can shift dramatically due to several factors including the selling price of other works by the same artist, the artist's continued or discontinued ability to produce new works, the historical significance of the piece, the reputation of the galleries or dealers that have a share in the artist (as representatives or holders of other works), the piece's individual history, and general media hype about the artist him/herself. Therefore accurately predicting the value of a work can be difficult. Some see these fluid market changes as an opportunity to manipulate the market, but given the complex nature of the art market and its fragile infrastructure of ego and speculation, this opportunity can soon become treacherous. Further, there are many who believe that the practice itself of turning work into a commodity can strip the work of all symbolic and cultural value, which can significantly alter its desirability on the market. Even if a work is "worth a lot", it is actually worth nothing if no one else is willing to buy it from you.

In reality, after seeing the statistics on the failure of art funds, I might not see this as enough of a viable option for making money and would forego the opportunity entirely. However, if I did decide that I wanted to try my hand at a market were others had been unsuccessful, it would have to be carefully plotted and full of fallbacks in the case of market failure. Like a good portfolio, I think it would be important that the fund be diversified. All though this might limit the overall profit of one sector which is highly successful, it would also mitigate losses if the other end of the spectrum should arise. To diversify the portfolio it would be important to have several different genres of work, work from a range of time periods, and artists of varying levels of fame and repute. The art would be collected as follows:

15% old masters and Renaissance/Baroque period work (50% painting, 20% drawing, 30% sculpture/structure)

25% contemporary art (40% painting, 20% sculpture, 30% print, photography, new media, 10% film)

30% impressionist/ modernism

15% antiquities

15% old masters (non-western/Asian, Indian, Middle Eastern, African regions)

My fund's strategy would have to employ an array of marketing, advertising, and commercial activities to ensure the longstanding value of the work held. Work held in the fund would be loaned for a percentage of its purchased value to members of the fund for no longer than 1 year with insurance, loaned to major museums and institutions with solid reputations, loaned to galleries for temporary exhibition, or loaned to collectors with reputable collections. Selected works would be put on exhibition, specifically curated to highlight the cultural value of the work held by the fund, which would be open to public viewing, media coverage, entrance fees. Media coverage of artists represented by the fund would be highly encouraged, and the fund might even publish its own books or informational publications to inspire faith in the stability of the fund and its artists.

The work in the fund would be acquired from "distressed" sales of work being sold at low prices by collectors, galleries, or even museums in need of capital. It will be held by the fund for no less than 10 years, at the end of which time all work will be sold from the fund in a series of 5 auctions, each covering a particular category of art held. These auctions will be highly publicized before the event, and will be by invitation only to increase exclusivity and potential price ranges of work by competition and feelings of "now or never". Investors in the fund would be able to invest a minimum of 10,000 dollars, with hopes of 10-15% returns.

Some art the fund would hope to acquire would include:

Donatello

http://karlzipser.com/mich1jpg/haman2.jpg

Michelangelo

http://jameswagner.com/mt_archives/Chris_Martin_Glitter_Painting.jpg

Christopher Martin

http://4.bp.blogspot.com/_XZfUU_433lQ/TOGA8JWv7LI/AAAAAAAAAzs/hpLQdRzKTJk/s320/picasso33.JPG

Pablo Picasso

http://www.artinamericamagazine.com/files/2009/10/26/img-kraus-1_173038618769.jpg_standalone.jpg  http://www.artinamericamagazine.com/files/2009/10/26/img-kraus-1_173038618769.jpg_standalone.jpg

http://www.artinamericamagazine.com/files/2009/10/26/img-kraus-1_173038618769.jpg_standalone.jpg

Kitty Kraus

http://theartblog.org/blog/wp-content/uploaded/nickcave-300x225.jpg

Nick Cave

Investing art is a practice that is poorly understood largely due to its controversial nature3. Art investment is looked upon as a mechanism that strips art of its cultural and creative meaning and transforms art into a purely money making strategy. It was interesting to learn about the development and occurrence of different art investment funds and strategies and see the different factors that were considered during the development of certain investment plans. During certain time periods, there were unique threats to the success of some art investment funds and it was very interesting to see how certain investment managers and investment strategies were created to counteract possible failure of their investment portfolio.

If I were to create my own investment fund, I would employ a variety of strategies and utilize multiple investment vehicles2. I would use a “showcasing” strategy, which would seek to increase the funds in my art investment portfolio by placing my works in important museum shows2. The exposure of the art can help to attract more money to my fund. In addition to that method I would use a “distressed art” strategy in which I would acquire art at significant discounts from collectors who are selling due to the likelihood of bankruptcy or insolvency2. I would also try to make sure that within my collection of fine older art, I would include new artists as well. In doing so I would adopt the “emerging artists” strategy and center my investments on new artists in the art world who are not yet established and therefore have the potential for rapid price appreciation. Because art investments are typically long term, I would possibly try the “buy and hold” strategy and hold on to artworks hoping that with time and a consistently good market, I can earn some return. If this strategy becomes unsuccessful within a few years, I may forgo it and adopt another one. The same goes for if any of the other strategies mentioned fails quickly. Using these four strategies would hopefully garner some success and money within my investment portfolio. Also, I would have a US based investment vehicle and one located abroad (likely in the British Virgin Islands because it’s a common offshore fund region and investor-friendly region2, 3). This would allow me to take in monies from both domestic and foreign sources. My art investment fund, like most others today, would likely resemble a private equity fund or hedge fund in terms of its structure and operation.

If feasible, the artwork collection in my investment portfolio would consist works from classic artists like Pablo Picasso, Henri Matisse, Salvador Dalí, and Rafael. In terms of contemporary art, I would look to include artworks from Damien Hirst, Jeff Koons, Horace Pippin, and Henry Ossawa Tanner, for their thought provoking pieces. Emerging artists like William Wray and Caroline Marine, would inspire how I approach and include emerging artists in my pieces. My collection would consist of paintings mostly, but there would be sculptures, photography, and other forms of art from these artists and those similar to them. I would definitely want attention to my pieces, to garner more funds on investments.

Sample Painting by Caroline Marine:

Sample Painting by William Wray:

References:

2http://www.artfundassociation.com/_what_are_art_funds/basic_af.html

http://www.artfundassociation.com/_what_are_art_funds/basic_af.html3Horowitz, Noah. Art of the Deal: Contemporary Art in a Global Financial Market. Princeton, NJ: Princeton UP, 2011. Print.

The interesting thing about art funds is that their focus is almost all about art as a means of making money. Unless, for example, an art fund publicly displays its holdings or allows investors to temporarily borrow a work, the art fund basically treats art as nothing but an “asset” which will hopefully turn a profit. In other words, the goal of the fund is to achieve significant financial benefits to investors (Horowitz, 156-57). But what I find most interesting about an art investment fund is how the fund’s holdings are valued. When it comes to a publicly traded stock or a mutual fund, there is an open and transparent means for buying and selling which sets the market price. But that is not exactly the case with art investment funds.

For some art funds, such as artfonds-21.com, referenced by Horowitz in Appendix C, the goal is a publicly traded stock corporation that will provide a measure of value in the market place for its holdings.

Without some sort of publicly traded equity in the investment fund, the investor in an art fund must rely on expert valuations, such as the detailed appraisal Professor Finley provided the Tosca Fund in 2011.

What I found very interesting about the Professor’s appraisal is that in valuing a fund, one has to rely on a lot more than auction prices. I had originally thought Thornton’s assessment that art is worth what “someone is willing to pay for it” as an easy gauge of value. But it’s overly simplistic; many more factors are in play and need to be considered, e.g., uniqueness and history of the work, given the reality that not every piece is readily auctioned or sold.

Interestingly, the increasing popularity of art investment funds is in and of itself a gauge of the stabilization art values since the start of the recession (as well as a reflection of renewed confidence in the funds after many of them closed down ). One recent fund, known as the Art Exchange, was started last year. In its brochure, which refers to the company as “The Stock Exchange for Art,” it lists its attributes as:

Here is the link to their brochure: http://www.afmarkets.net/en/brochure.pdf

With the art market, there has always been an issue of concern with transparency. In order to address that concern when it comes to art funds, the Art Fund Association was started in order to educate the public as to all aspects of the art market. http://www.artfundassociation.com/

Given that the Association needs the funds to survive, I wonder whose interest it considers more important – the investors or that of the funds?

Investing in an art fund has come a long way since the model of the British Rail Pension. While the funds had some great success, there has also been multiple cases of funds closing down. It can’t be easy to establish a profitable art fund. If I were to try to design an art investment fund, I would first focus on establishing a fund that acquires artwork which is part of a small niche, which, while not very diversified, would make it more easily to market to potential investors. What comes to mind is some aspect of the contemporary art market, let’s say, the works of contemporary artists live in New York State. I’d call it the Empire State Art Fund. I would try and condition management fees, appraisal fees, and investor return on the existence actual profits from sales. In other words, aside from essential operating costs, no one involved in the fund makes any money until there is an actual and realized profit. At that point, there would have to be an equitable distribution of a portion of the profits .

The highlights of the fund would be something like this:

THE EMPIRE STATE ART FUND

- Only acquiring contemporary works (of all kinds – paintings, sculptures, etc. ) from artists based in N.Y. State. (Seeking to establish a following and loyalty amongst NY artists and NY art investors).

- No acquisitions in excess of $10,000. (Creating the possibility for a large return on investment and establishing interest by focusing on works that are not yet well known).

- Maintain, as noted in Dr. Finley’s Toscafund Report, a “thoughtful and strategic acquisition policy.”

- Minimum investment of $1,000 – closed end and private - amount invested determines amount of equity in the fund (making it easy for many to participate and invest in the fund).

- Any works can be borrowed from the fund for a short period of time (as long as insurance is in place).

- No returns (for advisors, management or investors) until the fund makes an actual profit (establishing integrity).

- Any sales to be conducted on line at the fund’s own web site. (no sale commissions).

- Monthly statements of all activity (complete transparency).

- All finances to be handled by a public accounting firm. (Create integrity so investors have trust)

Example acquisitions:

1) Christa Toole

Oil on Canvas

“Gravitational Wave”

Acquisition Price $1500

2) Soos Packard

Sculpture

“chickn lickn head”

Acquisition Price $2500

3) Kelso Jacks

Painting

“Prey”

Acquisition price: $750

From the reading it seems that Art Investment Funds are definitely a risky way to invest. The funds have rarely been successful with the exception of the British Rail Pension Fund created in the 1970’s which really was not even as successful as it appeared. While in theory investing in art may seem like a sure way to make money, the uncertain and volatile nature of art value has shown it to be much less straightforward. The continued interest in this type of investment is curious given its history of failure.

I find the idea of Art Investment Funds disturbing in its lack of regard for art’s intrinsic value. Even more than anything we have seen thus far, the Art Investment Fund is concerned with nothing more than art’s monetary value. The comparison between real estate and art investment was also concerning. How can we guarantee that a bubble is not being created that will eventually pop? I also noticed that some of the funds allow their members to display the art from the funds in their homes. This seems like another significant risk, what if a piece is not cared for properly or accidentally destroyed? What if a member has a piece of art and the fund fails, does the member get to keep the art? What if they refuse to return it in order to regain at least some of what they invested? While I’m certain that the works are insured and the members have signed contracts that stipulate how everything will function, it still seems like there is a high potential for problems.

While the Tosca Photography Fund seems to be functioning acceptably, I certainly would not invest my money in an Art Investment Fund unless more evidence of stability could be presented. Speaking hypothetically, if I did invest, I might do the following:

1- Buy lesser known works by established non-living artists.

2- Buy works from contemporary artists on the verge of success, before the price for their work become excessive.

3- Make sure to mix the type of art to include paintings, photos, and sculptures in an attempt to diversify the portfolio and hopefully better the chance of returns.

4- Limit the number of investors in an attempt to maximize individual returns.

5- Hold the works until their value appreciates considerably.

Here are a couple examples of the kind of works that I would try to acquire for the fund:

A work by an established non-living artist:

Diego Rivera’s “Mujer Bañandose” which recently sold for $116,500 at Sotheby’s but I think has the potential for a higher value in the future.

A work by an emerging artist:

Adam Pendleton’s “System of Display, E (ETERNAL/Against/Jean-Luc Godard, Le Grand Escroc, episode from Les Plus Belles Escroqueries du Monde, 1964)” which was displayed at Art Basel 42 in the Art Statements section.

Unable to render {include} The included page could not be found.

While most dealers, galleries, and collectors want to distance themselves from the commercial side of art and give genuine, pure love for art as their reason for selling, buying, and collecting of art, art funds operators or managers exhibit an openly money-oriented attitude toward art. After all, their goal is to maximize the rate of financial return on artworks in their collection.

An industry still at its developing stage, art investing has several advantages. Art funds are more immune to external factors like economic crises. Because art funds buy and hold on to the artworks, they are less susceptible to fluctuations in the market (Horowitz 148). Even during inflationary times, a work of art will still be worth something, whereas company shares often become worthless (Horowitz 148). Also, since the art market is “fragmented and hybrid,” a decline in price of works in one sector does not mean the same for another sector (Horowitz 148).

In Tosca Photography Fund’s year end report by Professor Finley, it is revealed that many factors affect the valuation of artworks, among which are rarity, historical and intellectual weight, uniqueness, subject matter, provenance, exhibition history, printing dates, and medium (Finley 4,5). For photography in particular, printing in editions lead to the decrease in value (Finley 4). Often times, the prices of works by other comparable artists are helpful in determining the value of an artist’s work (Finley 5).

If I were to establish an art fund, the basic design would be as follows:

1. Target for an annual return of 10-15%.

2. Diversify: Buy art in four different categories: 1) Old Masters, 2) Impressionist art, 3) Modern art, 4) Contemporary art.

3. Set the minimum contribution at $250,000.

4. 2% will be taken off for overhead and operational costs and20% for performance fee on earnings.

5. Have a lock-up period of 10 years.

6. Profits will start be distributed after the third year.

7. Lend art pieces to museums or important exhibitions to reducing storage and insurance costs add provenance and boost resale price (Horowitz 150). Lending works to exhibitions will also increase publicity. When prestigious magazines and newspapers write reviews on the works, their value accrues (Finley16).

8. Provide investors with yearly statement of professional appraisal of the art in their portfolios for confidence and integrity.

In such industry as art investing in which decisions are largely dependent upon the course of the market and auction, market analysis will be key to obtaining success when it comes to re-selling. Respected art appraisers and advisers will be of critical importance.

Moreover, apart from the most central guidelines laid down as above, the Tosca Photography Fund seems to have benefitted from carrying out retrospective exhibitions and private events as well as publications. Exhibitions and private events will help foster solidarity among investors, and publications will increase the chance of sale of the works included in the book. Negotiating with auction houses to drive the commissions down can also help in securing more profit and incurring less cost.

Sample works I would buy:

Gustave Caillebotte. The Man on the Balcony.

https://encrypted-tbn0.google.com/images?q=tbn:ANd9GcTkOhHlX0Xa98NeJCE_LzpKOOvy46KR0Kn7pHG9YArKxWNJs7vR

Geraldine Gliubislavich. Untitled. 2009.http://www.vegasgallery.co.uk/wp-content/uploads/2010/09/untitled-42.jpg

Name of Fund: Art Politico

Fund Overview: Contemporary Photography and New Media Art (both with a focus on contemporary political issues)

Investment Details: Target- $100 m ($75 m institutions), Term: 10 years

Fund Description: Target Returns o f 30-40%

This investment fund will use a diversified strategy and focuses on two market sectors: contemporary photography and emerging new media art. A focus on political issues is the underlying characteristic that will tie the two sectors together. This focus intends to add insurance to the value of the works through their cultural and historical significance.

The optimal allocations for each sector are: photography- 70% and emerging new media art- 30%. This structure of allocations is meant to use contemporary photography as a base, as the photography market has done especially well in recent years and is expected to continue to do so, based on Tosca Photography Fund's 2011 Analysis [4]. New media art acquisitions will be of higher risk, but with the expertise of the advising board, these investments are expected to generate proportionally higher payoffs.

This summary projects that investments will be made until year four, and divestments will be made from years three to ten. These fund will target about $75m or 75% in institutional investments, creating complex financial ties not possible solely with individual investors. For financial security, any purchase greater than 10% of the funds commitments will be subject to approval by the Fund Board. The fund will be registered in the British Virgin Islands to avoid capital gains taxes. The difference saved will be reinvested toward future purchases.

An additional financial strategy will be to loan the works out on exhibition. By placing works with prominent art institutions, the works will acquire another layer of history and cultural value. This strategy is intended to help boost resale prices.

Hiding in the City, by contemporary Chinese artist, Liu Bolin, is an example of the fund's photography investments. For this series, Bolin takes photographs of himself camouflaged to blend in with urban landscapes.

[1]

He intends for his works to show the effects of the city on the people living in them. The works have a strong political agenda. He states, “I experienced the dark side of society, without social relations, and had a feeling that no one cared about me. I felt myself unnecessary in this world. From that time, my attitude turned from dependence into revolting against the system.” [2]. He also uses his work to protest against artistic persecution. He continues, “...contemporary art was in quick development in Beijing, but the government decided it did not want artists like us to gather and live together. Also many exhibitions were forced to close.” [2].

Mona Lisa Meta-data is an example of the new media art that the fund would focus on. The piece was shown at the Second Annual International Art and Science Exhibition and Symposium in Beijing. Users can alter the iconic image by using newly developed optical tracking technology, in which that stated purpose is to “offer one possibility for an even more transparent interface” [3]. But the work also brings into focus larger political issues, such as the dominance of the West and globalization [3].

[3]

Thus, it is works like these that the fund will focus on due to the added value of their social and historical commentaries. While the new media art category is less defined and more volatile, the Art Politico Fund will try to capitalize off its emergent status, as another chapter in the history of artistic development.

Sources:

[1] http://v1kram.posterous.com/liu-bolinthe-invisible-man

[3] http://magazine.art-signal.com/en/one-cache-memory-of-new-media-in-china/

[4] Tosca Photography 2011 fund review.pdf\

Art funds are a very interesting concept because they are solely interested in the monetary value of the art, thereby they profit from the sales of art, but not in the same manner that a dealer does. Art Funds require less space to show their pieces of art, and have lower costs overall than dealers do. At the same time, Art Funds are entirely dependent on a successful sale of their piece, which may fluctuate based on economic problems in society. However this is not as large of an issue, as this is buffeted by the social value of art. Art demonstrates an elevated status in society, and thus the wealthiest people in society are the ones shelling out millions of dollars to these Art Funds, and these people rarely are that affected by economic change, and thus will continue to purchase art that elevates their social and economic status.

Nevertheless, Art Funds are subject to volatile sales, as determined by the demand for a certain piece. The money an Art Fund makes, is made through resale of a piece of art. Thus, people who manage Art Funds must decide that something is worth more money than it is being sold for, buy it, and resell it at a greater cost. This is always a gamble. One could overestimate the demand for a certain piece, due to either the market already having too many similar pieces, or general indifference to a piece. Thus, in this situation, the best thing to do is to hold on to the piece until demand is increased, however this means no money coming in, and negative cash flow. I believe that Art Funds may decrease the Art Market, because of its solely monetary based nature. This is making it into a consumerist, industrialized market, where there is no appreciation for uniqueness or outlandish art, but only for that which will sell. Also, it puts too much control in the hands of the people who run the Art Funds, because as they have to ability to hold onto pieces until they will be worth more, they will be able to completely control the art market, dictating what is popular at the time.

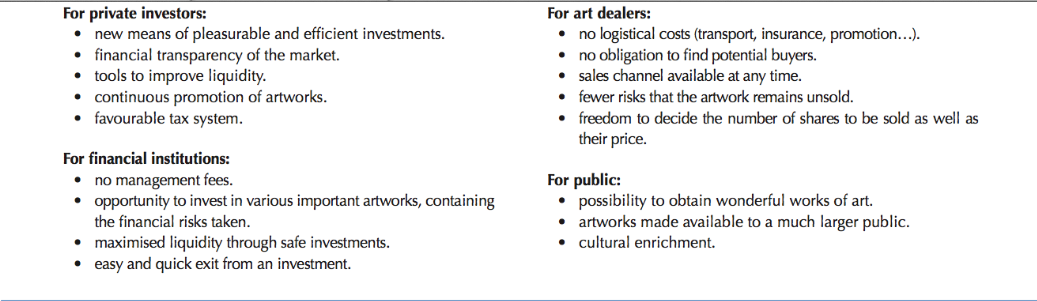

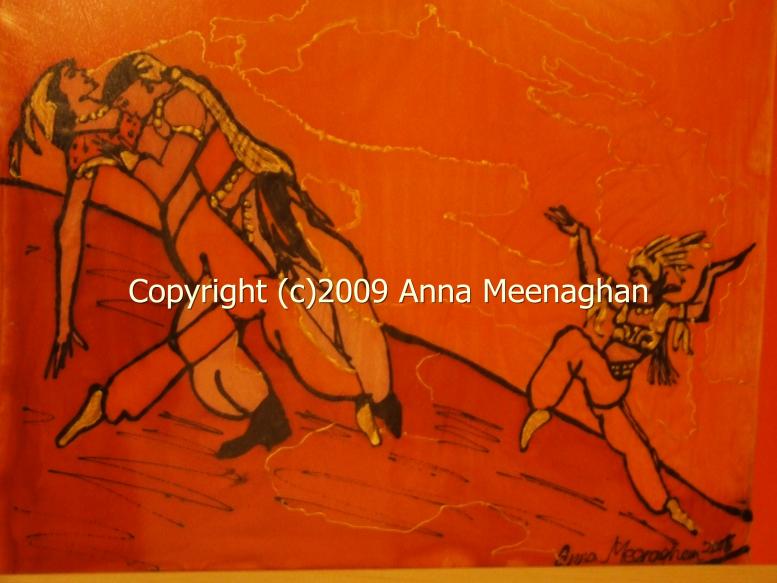

However, if I were to create my own investment fund, I think the most important thing I could do would be diversify. By limiting myself to a certain area of art, I could be harming my business because it is always uncertain when a certain type of art will become obsolete. By having a diverse portfolio of paintings, photography, sculptures etc. etc. I believe I would have the best chance of success. Also, I would employ the same methods that the Tosca Photography Fund employs in advertising. By garnering press interest in my pieces, I would be more likely to sell them. I also would place some of my pieces in museums or galleries to increase the chance that they will sell by providing a place where they will be exposed to potential buyers. For my art fund, I also would diversify the artists, and their level within the art market. I would buy pieces from already known artists, to demonstrate my knowledge of the art world, and also buy pieces from lesser known artists that are similar to the successful artists I already own pieces from. The pieces from artists who are already successful may not sell for much more money than I paid, however it would be a good way to bring in art enthusiasts, and then introduce them to new artists who have not been exposed yet. It is through the new artists that I will be able to make the majority of my money. I would focus my efforts on whatever art style was most successful, and new at the time. For example, right now I would focus my art fund on pieces that are contemporary, because it is at the forefront of the art world right now, and thus would be easy to find new artists such as Jessica Jackson and Anna Meenaghan.

Pieces by Anna Meenaghan:

Pieces by Jessica Jackson:

Art funds are investment vehicles that, like hedge funds and private equity funds, exist to provide substantial commercial rewards to those who provide the capital that allows acquisition of the art and to those who manage the fund. In practice most managers draw on a range of advisers and specialist service providers. The interests of those three entities are not necessarily identical.

Although art funds deal with objects that may be described in many ways, it mostly represent unique aspect of a nation or region's cultural patrimony and may be as considered priceless to those fund them. They aim to maximize the rate of return on works in their collection.

Sale of works acquired by a fund may occur progressively throughout the life of a fund - with returns being useful in purchase of works that will provide greater returns in future and in securing participation by additional investors. In the reading what I came to understand was that although the market value of particular art work may increase, the market value of other assets will often increase at a greater rate in the long term; for example

buying a Picasso or Leger oil in the 1950s would produce a respectable profit when that painting was sold thirty or fifty years later.

If I were to establish an art fund first I will develop some strategic plans. Firstly, I will develop a plan to trade recognized major works, for example paintings from masters such as Pablo Picasso which are recognized to have significant oeuvre and therefore are very likely to appreciate in value faster. In doing this I will have to carefully analyze the market, as there seem to be an uncertain rise and fall in prices of some famous well-known artist. So I am not going to get works just because the artist in famous, but because of the quality and nature of the works of the artist. The second strategy I will take will be to acquire, hold and then sell works that are more clearly undervalued. These will be works by artists who are recognized as important but not on the level of being classified as first rank-it will also include artist who are yet to jump from commercial galleries to more acclaimed national collections and genres. It may seem as a risky strategy, because it is depending on the hope that in some years to come it will sell at higher price, however, it is likely to be more profitable than buying a recognized masterwork and trusting that demand for that work will inevitably push up its value.

In making a design for my fund, I will

- Spend time on choosing the works that will benefit the fund and in turn bring in some profit and revenue for the company.

- I will very much consider the issue of globalization and diversity, and take on some very interesting pieces from different part of the world, like china, middle east parts of Africa and constantly exhibit them in galleries and museum so that they tend to become very frequent images in the eyes of collectors, critics, and the general public. That way they will attain some positive notoriety and may just begin its way to be a high value art

- I will invest in different mediums of art, painting, sculpture, drawings, installation, music, dance choreography etc. this is because I want to encompass the wholeness of art and effect that can emerge if the are placed side by side

- As I take a look at where the world is going to, I will be very much un-reluctant to acquiring works, which are deeply immersed in new media technology, yet have strong roots and connection to traditional art forms. In a world that is constantly moving toward a more technological and digital age, I believe that in due that these will become very much appreciated and will fetch some good income and profits.

- My priority in this fund is to make sure that art is being appreciated for its content and meaning, therefore, My expectancy for profits and sale and monetary input will be at a high of $25 million for the first 5 years.

- Finally, I will take on young artist with great potential for their artistic career, and put them in shows for proper exposure.

My hope is that the system I have proposed will span through the timeline of art and its importance to help bring a better meaning to what art investment funds are all about.

This is an example of works that the fund will invest in. the names of the artist are below:

- Pablo Picasso

- Yue Minjun

- James Turrell

- Alexa Meade

- Ato Delaquis

- Rembrandt

Unable to render {include} The included page could not be found.

The success of an Art Funds is absolutely dependent on the resale value of the artwork. Thus, the management of an Art Fund must see a “deal” meaning the work is being sold for less than it’s worth or that it could increase in value over time. Possible problems in accumulating art could be overestimation in an artworks value or lack of demand or appeal for the artwork. Thus, it is important for the fund to consider holding onto the piece until the demand increases. Because Art Funds turn the art market into an industrialized market, there is little to no appreciation for uniqueness or outlandish art, but only for art that will have commercial success. In my fund I would accumulate art that would have commercial success but I would also invest in more obscure art that would not necessarily have a wide appeal but would be appreciated by more daring buyers.

As prices are generally hard to predict and are subject to buyer's preferences, this makes resale value difficult to ensure. Therefore it is important to invest in up and coming artists where the seller is able to name a price without being subject to the comparison of other works that have been sold. I would consider that the value of art depends on its uniqueness and scarcity. In order to create a stable, viable and successful art investment portfolio I would consider the following strategies:

- Accumulating diversity in mediums, genre and notoriety of the artists. If my fund were to focus exclusively on contemporary art or old masters I would be limiting the collection’s worth.

- By creative a diverse collection of artwork including art from many movements, I could maximize the value of the collection by appealing to many different audiences and being involved in many areas of the art market.

- Diversity in notoriety of artists is also important in establishing a successful art fund. It is important to have very famous and well known works but also important for the fund to invest in up and coming artists.

- In particular I would invest in old masters that are fairly limited in quantity and can no longer be produced. Specifically, I would invest in Rembrandt’s work because he is an extremely brilliant artist who has worldwide appeal. In addition to his global recognition I believe Rembrandt’s work will increase in value over the next couple years as enormous amounts of money are being spent towards attributing and de-attributing his paintings. In particular, new technology has allowed the University of Amsterdam and the Rembrandt Research Project to re-attribute paintings that were previously thought to be paintings done by Rembrandt’s pupils. In addition, the Rembrandt Research project has de-attributed paintings hanging in both the Hermitage Museum in St. Petersburg and the Metropolitan Museum of Art in New which are now being called “School of Rembrandt.” In one particular case a private investor purchased a painting called Old Man with A Beard for $40,000 in 1998 which was sold as a work done by one of Rembrandt’s pupils. The Rembrandt was later re-attributed thanks to x-ray technology and a particle-accelerator as two paintings were found underneath. This painting is now worth $13 million US dollars in 2011.

- I would steer away from investing in Koons & Hirst as I think the appeal of their work is a fad and I believe the mass production of their artwork and prints will cause them to devalue over time.

- I will consider that contemporary art is at the forefront of the art market today and it is important to invest in what the public is interested in.

- I would invest in up and coming artists such as Jasmina Danowski whose paintings are very colourful and abstract. She is also a good candidate for investment as she uses both water-colour and oil. Artists that use different mediums are crucial as certain buyers may prefer one medium or another. Again, when searching for an up and coming artist it is important to consider how commercially successful the artists will be. I would choose Danowski as I believe she appeals to a wide audience and thus will have a huge resale value. It is important to invest in very “safe” artists that appeal to a wide audience and also to invest in perhaps one or two obscure artists who may not have as a commercial appeal but who create very special and unusual pieces.

- I would invest in a more obscure up and coming artist like Pasquale Cupari. His pieces are very unusual and he mixes many different mediums. I cannot see his paintings being very commercially successful but I think there are buyers who would appreciate and believe in the bizarre pieces he creates

- It is through the exposure of the new up and coming artists the fund will endorse that will generate the largest profit. If the fund hangs onto all it’s investments, the demand for each artist will likely increase after much promotion is done.

- I would also donate portions of the funds portfolio to a museum or other public foundation. This would expose the fund to a larger audience and make the public more aware of the type of works in the fund.

A Living Sound II by Jasmina Danowski. Ink and gesso on paper (60X 40 inches).

This painting is a good size and I believe it has huge resale value as I think it could appeal to many experienced buyers and buyers who are just starting their art collections.

Paparina by Pasquale Cupari. Oil, Enamel and mixed media on Canvas.

I believe this work is a little more obscure and will have less commercial appeal but will have have resale value to certain buyers.

Links to the very interesting Rembrandt reattributing stories:

The Art Investment Funds are a double-edged sword. There is much evidence pointing to the fact that these funds do not rise and fall with the equity market, and further are less prone to volatility. FAF founder, Phillip Hoffman states that a Canaletto will “never fall to zero”, however highlights the fact that stocks and bonds may fall to zero.

There are misconceptions about the degree to which art funds are safer than more mainstream investment funds. It is not the fact that art is a real asset that makes the fund safer than conventional products. The underlying art is what makes the fund safer. The difference between a Canaletto and the starving artist down the street is that the risk in paying $250,000 is far less for the Canaletto, despite the payoff being greater. The fund managers know exactly what they are doing. Often the managers have worked previously in finance and private equity. The funds are essentially private equity funds backed by art. The five to ten year horizon is interesting, as the fund managers can pick the absolute most opportune time to sell the work. Because these are closed funds based on one of a kind pieces, it is difficult to mark the fund to market, besides a professional valuation.

What I find most interesting is the investment strategy of these funds. Horwitz states that there are usually three strategies funds use: diversified, region specific, and distressed assets. As the art investment fund is still in its infancy, it is clear that many of these funds take a fairly conservative investment approach. Very few are focused on small name artists looking to hit the lottery.

If I set up an art fund I would call it the NK1 Fund and most likely take a diversified approach. I am weary of putting all the capital into art from one geographic area or one style of art. In the Tosca Photography Fund 2011, the fund’s head stated, “As seen in these sales, not every high ticket item sold, but perhaps that is not a bad thing as it indicates connoisseurship rather than exemplifying the vortex in which everything that is offered is absorbed by the market”. This quote explains that there is risk involved in the investment, however quality art collections carry more assurance with the current sophisticated collectors.

In my fund I would look for heavily undervalued contemporary pieces from masters, as well as low value not-yet famous artists. The low value masters would be used to hedge against risk. One example of this would be Picasso’s Les femmes d'Alger, version L. The painting recently sold for $21 million, well under its $30 million estimate. Using this strategy of holding big name pieces, I would also lend the art work out to galleries and museums for a few percentage points, hoping to further increase the value.

Among the diversified art pieces, my fund would also invest in new up and coming artists in hopes that over the longer period of time, their art would greatly appreciate in value. Finding lists and following the emerging art scene would be extremely important. However, taking a hands on role in choosing work would greatly benefit the fund. I would invest in artists like Colin Roberts, an emeging artist who works with Plexiglass (shown below). He has recieved recent noteariety, and a sharp increase in demand for his work could mean a great return.

The main strategy for my fund would be buy and hold (while putting the famous works in galleries). I believe that the small arbitrage transactions, and buying distressed work carries far more risk.

There are misconceptions about the degree to which art funds are safer than more mainstream investment funds. It is not the fact that art is a real asset that makes the fund safer than conventional products. The underlying art is what makes the fund safer. The difference between a Canaletto and the starving artist down the street is that the risk in paying $250,000 is far less for the Canaletto, despite the payoff being greater. The fund managers know exactly what they are doing. Often the managers have worked previously in finance and private equity. The funds are essentially private equity funds backed by art. The five to ten year horizon is interesting, as the fund managers can pick the absolute most opportune time to sell the work. Because these are closed funds based on one of a kind pieces, it is difficult to mark the fund to market, besides a professional valuation.

What I find most interesting is the investment strategy of these funds. Horwitz states that there are usually three strategies funds use: diversified, region specific, and distressed assets. As the art investment fund is still in its infancy, it is clear that many of these funds take a fairly conservative investment approach. Very few are focused on small name artists looking to hit the lottery.

If I set up an art fund I would call it the NK1 Fund and most likely take a diversified approach. I am weary of putting all the capital into art from one geographic area or one style of art. In the Tosca Photography Fund 2011, the fund’s head stated, “As seen in these sales, not every high ticket item sold, but perhaps that is not a bad thing as it indicates connoisseurship rather than exemplifying the vortex in which everything that is offered is absorbed by the market”. This quote explains that there is risk involved in the investment, however quality art collections carry more assurance with the current sophisticated collectors.

In my fund I would look for heavily undervalued contemporary pieces from masters, as well as low value not-yet famous artists. The low value masters would be used to hedge against risk. One example of this would be Picasso’s Les femmes d'Alger, version L. The painting recently sold for $21 million, well under its $30 million estimate. Using this strategy of holding big name pieces, I would also lend the art work out to galleries and museums for a few percentage points, hoping to further increase the value.

Among the diversified art pieces, my fund would also invest in new up and coming artists in hopes that over the longer period of time, their art would greatly appreciate in value. Finding lists and following the emerging art scene would be extremely important. However, taking a hands on role in choosing work would greatly benefit the fund. I would invest in artists like Colin Roberts, an emeging artist who works with Plexiglass (shown below). He has recieved recent noteariety, and a sharp increase in demand for his work could mean a great return.

The main strategy for my fund would be buy and hold (while putting the famous works in galleries). I believe that the small arbitrage transactions, and buying distressed work carries far more risk.

Unable to render {include} The included page could not be found.

Consider & comment:

Please use this space to respond to your classmates' work and to engage in lively discussions on the day's topic. Keep your comments concise and conversational by responding to others, rebutting or supporting their ideas. Use the comment box below for these observations.

3 Comments

user-75024

One major concern voiced by many in the class is the greater perceived risk of these funds. While I think there is some merit to to being concerned, the underlying assets are in some ways not so risky. Consider the fact that many mainstream investment options are also based on intangible/ speculative value. Sovereign debt- part of great speculation is just based on the full faith and credit of the country issuing the debt. Buying REITs is extremely popular, but besides the cash flow derived from rents and mortgages, the value of the properties are subject to mass speculation. I would compare it to a wine investment fund http://www.wineinvestmentfund.com/ . I think while it is risky to buy art, if one could create a collection with nearly a billion dollars of assets have a great deal of bargaining power in getting paid from loaning out the art. It would be similar to a large company paying a 3% dividend and hoping that the underlying assets appreciate in value. The famous art pieces will always bring a small return in terms of gallery showings, however what I think will really bring the returns are small artists which funds buy at bargain prices and hold for the long haul.

user-9c486

Nicholas, I think you make an interesting point about risk. But it seems that concern is somewhat warranted when so many of the funds have closed. While that may have been a product of the recession and problems with financing, it still does not seem easy for a fund to be successful. Not only is the artwork a speculative investment, there are so many other variables, for example, management fees, storage fees, insurance, etc. I’m also not so sure about how easy it would be to loan out the art work in return for a fee. Are that that many people, galleries or museums out there that are willing to pay a fee to rent a piece of art?

I think that one of the most important ingredients for any art fund to be successful is an expert appraisal / valuation, such as the one the Professor did for the Tosca Fund. Without that kind of detailed appraisal of a fund’s holdings, it seems to me that investing in art funds is risky business.

Cheryl Finley

Thanks, all, for your proposals for art investment funds, which are indeed novel and fascinating. I like the tight focus on some of your funds -- i.e. on New York only, or contemporary artists only, or global emerging artists only. The examples of the actual works you would acquire are also eye opening. Many of you discussed the working mechanisms of art fund and were concerned about the art funds that merely 'held' the art in the funds as 'assets.' That is, those funds that didn't do anything really to promote the work or the reputations of the artists in their funds. As some of you have pointed out, that was not the investment strategy of the Tosca Fund. In fact, many of the works in the fund were exhibited in major museum and in gallery exhibitions. Catalogs were written and symposia were held to educate people about the work in the Fund and over time educational efforts such as these increase the exposure for the fund and the work it holds -- and this, in turn, affects the value of the individual works held. Risk is a huge factor for anyone who might invest in an investment fund, whether it's technology or art. But knowing the investment strategy, the portfolio manager, and the end game are some ways to minimize risk. To be sure, it's important to have a portfolio manager who is knowledgeable about the kind of art that is being acquired for the fund. Great work all.